MY BLOGS

AFFORDABILITY CALCULATOR

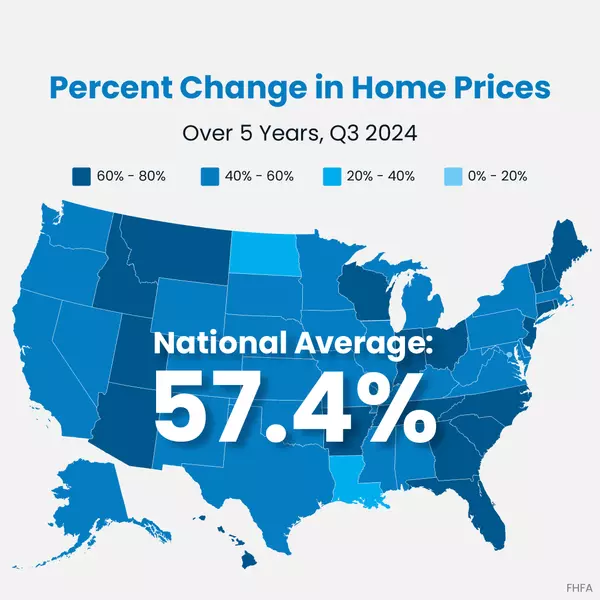

Quite affordable.

EXPLORE OUR FEATURED AREAS

How to Dispute Experian Credit Report Errors: A Complete 2025 Guide

Correcting Errors: A Step-by-Step Guide to Disputing a Derogatory Item on Your Experian Credit Report If you've discovered a derogatory mark on your Experian credit report that you believe is inaccurate, you have the right to dispute it. The Fair Credit Reporting Act (FCRA) mandates that credit bu

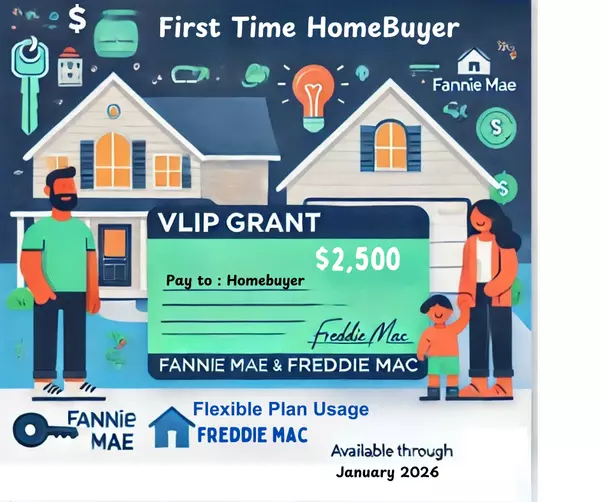

First Time Homebuyer : $2500 GRANT

Effective April 2025, FHFA grants have been suspended immediately. Programs and funding opportunities are constantly evolving. Staying informed and taking action when opportunities arise is essential for building wealth. Contact a Real Estate Strategist to explore current opportunities and maximize

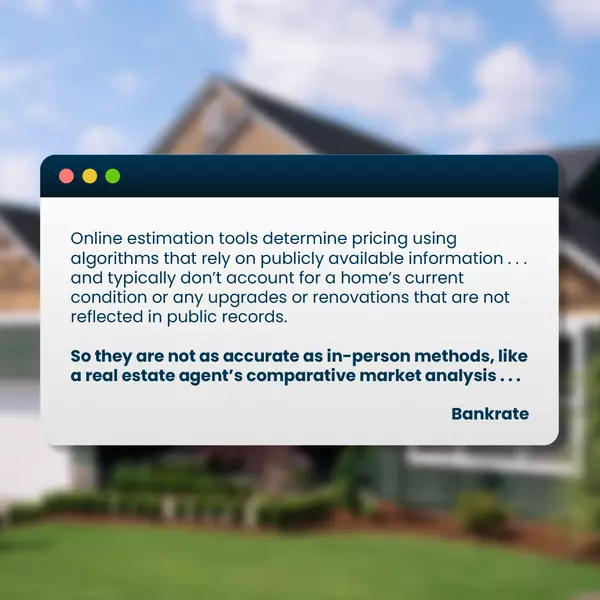

The Limits of Online Home Valuation Tools Bankrate Quote

Don’t rely on online estimates to figure out what your house is worth. While they’re definitely convenient, they’re not 100% accurate. That's because they don’t include key details like your home’s condition, updates you’ve made, and what’s happening right here in our local market. Want to know the

Categories

Recent Posts